What is ASC 606?

Written by Arnon Shimoni

✓ Expert

Last updated on:

ASC 606 is the revenue recognition standard under US GAAP, issued by FASB in May 2014 and effective for public companies starting fiscal years after December 15, 2017. It establishes a single, five-step model for recognizing revenue from contracts with customers, replacing more than 100 pieces of industry-specific guidance that existed under previous US GAAP. IFRS 15, issued by the IASB at the same time, is the international equivalent.

Both standards came out of a joint FASB/IASB convergence project.

Field | Detail |

|---|---|

Full name | ASC 606 - Revenue from Contracts with Customers |

Issued by | FASB (Financial Accounting Standards Board) |

International equivalent | IFRS 15 (issued by IASB) |

Effective date, public companies | Fiscal years after December 15, 2017 |

Effective date, private companies | Fiscal years after December 15, 2018 |

What it replaced | ASC 605, SAB 104, SOP 97-2, ASC 985-605, and ~100 other industry-specific rules |

Core framework | Five-step revenue recognition model |

Applies to | All entities entering contracts with customers for transfer of goods or services |

Key concept | Performance obligations |

Most affected industries | Software/SaaS, telecom, construction, media, healthcare |

What does ASC 606 actually require?

ASC 606 requires companies to recognize revenue when (or as) they transfer promised goods or services to a customer, in an amount that reflects the consideration they expect to receive in exchange. The standard does this through a single five-step model that applies to every industry and every type of contract.

The standard replaced fragmented, industry-by-industry guidance with one principles-based framework. Before ASC 606, a SaaS company recognized revenue using SOP 97-2 software rules. A construction company used ASC 605-35 percentage-of-completion rules. A real estate company used ASC 360. Each industry had its own playbook, and comparing revenue across industries was apples-to-oranges. ASC 606 collapsed those playbooks into one.

The most consequential change for modern software and AI companies: the introduction of the performance obligation. Under ASC 606, revenue is recognized when a performance obligation is satisfied, not when cash is collected, not when an invoice is issued, and not on a straight-line schedule by default.

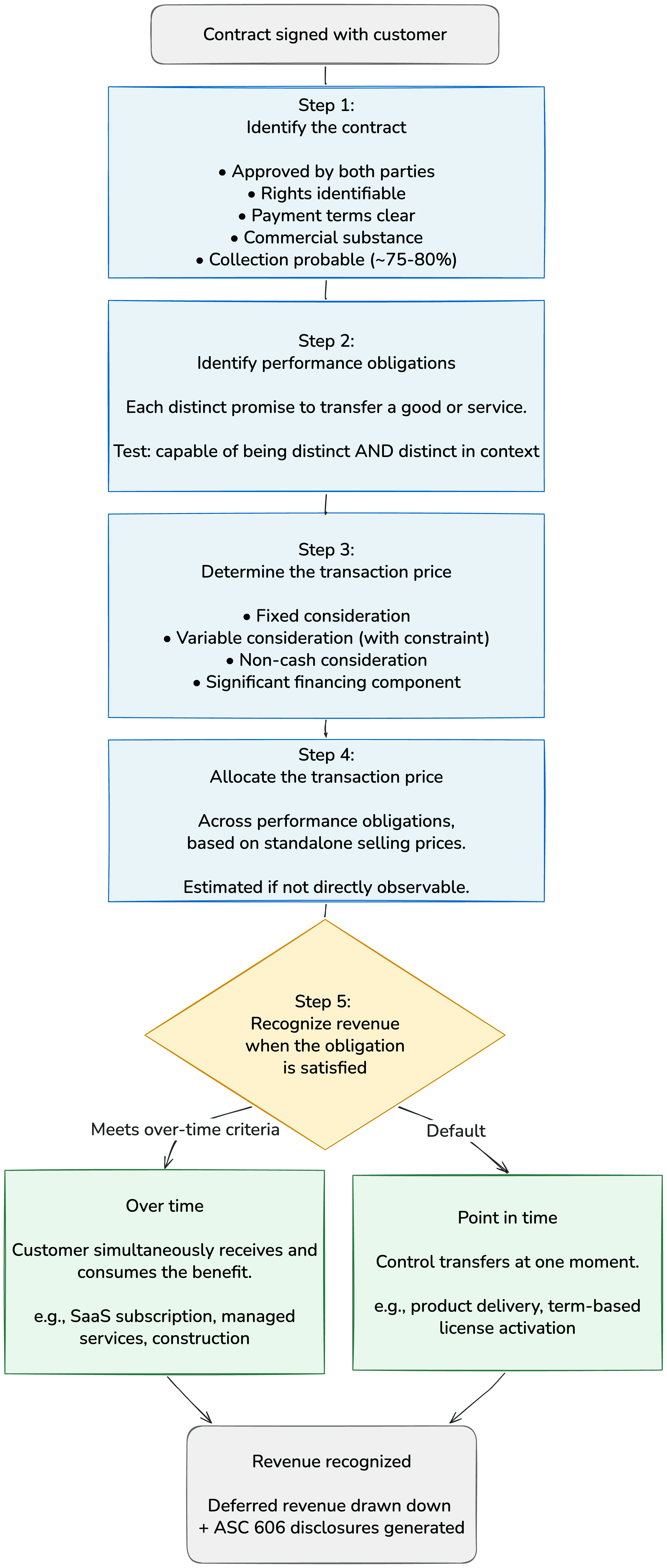

What is the 5-step revenue recognition model?

The five steps run sequentially. Every revenue arrangement gets evaluated against all five.

Step 1: Identify the contract with a customer

A contract exists when both parties have approved it (in writing, orally, or through customary business practice), each party's rights are identifiable, payment terms are identifiable, the contract has commercial substance, and collection of the consideration is probable. "Probable" under US GAAP means ~75-80% likely. This is one of the meaningful differences from IFRS 15, which uses a lower "more likely than not" threshold (>50%).

Step 2: Identify the performance obligations in the contract

A performance obligation is a promise to transfer a distinct good or service to the customer. The test: is the good or service capable of being distinct, and is it distinct in the context of the contract? If yes, it's a separate performance obligation that gets its own revenue recognition treatment. A multi-element SaaS contract (license + implementation + support + training) often contains multiple performance obligations.

Step 3: Determine the transaction price

The transaction price is the amount of consideration the entity expects to receive in exchange for transferring promised goods or services. This includes variable consideration (rebates, refunds, performance bonuses, usage-based fees), non-cash consideration, consideration payable to the customer, and the effect of significant financing components. Variable consideration is estimated using either the expected value method or the most likely amount method.

Step 4: Allocate the transaction price to the performance obligations

When a contract has multiple performance obligations, the transaction price is allocated to each based on standalone selling prices. If a standalone selling price isn't directly observable, it's estimated using the adjusted market assessment approach, the expected-cost-plus-margin approach, or the residual approach (in limited cases).

Step 5: Recognize revenue when (or as) the performance obligation is satisfied

Revenue is recognized when control of the good or service transfers to the customer. This can be over time (the customer simultaneously receives and consumes the benefit, the entity creates an asset the customer controls, or the entity's performance creates an asset with no alternative use plus a right to payment) or at a point in time (everything else).

SaaS subscriptions typically recognize over time because the customer consumes the benefit as the service is provided. Term-based perpetual licenses often recognize at a point in time, on the date access is granted.

How is ASC 606 different from IFRS 15?

ASC 606 and IFRS 15 came out of the same joint project and share the same five-step model. They are deliberately convergent. The differences are at the edges, and they matter for any company that files under both standards or operates internationally.

Topic | ASC 606 (US GAAP) | IFRS 15 (IASB) |

|---|---|---|

Collectibility threshold | "Probable" = ~75-80% likely | "Probable" = more likely than not (>50%) |

Shipping and handling | Accounting policy election to treat as fulfillment cost | Must evaluate whether it's a separate performance obligation |

Sales taxes | Policy election to present net | Must evaluate whether collected as principal or agent |

Non-cash consideration | Measured at fair value at contract inception | Measured at fair value at contract inception (similar in practice) |

Licenses of IP | Different timing for some renewals | Generally similar treatment |

Disclosures | More prescriptive (especially for public entities) | Less prescriptive |

Contract modifications | Same model, minor practical differences | Same model, minor practical differences |

Impairment of contract costs | Specific guidance under ASC 340-40 | Refers back to IAS 36 |

For most SaaS and AI companies, the practical differences are minor. The five-step model produces nearly identical revenue numbers under both standards. The differences show up in disclosure depth and edge-case scenarios (shipping fees, sales tax presentation, certain license renewals).

How is ASC 606 different from legacy US GAAP?

Before ASC 606 became effective in 2018, US GAAP revenue recognition was a patchwork of guidance built up over decades. The big sources of authority were ASC 605 (general revenue), SAB 104 (SEC staff guidance), SOP 97-2 (software), ASC 985-605 (software-specific), and dozens of industry-specific rules for real estate, construction, healthcare, franchising, and others.

What changed in 2018:

Principles-based, not rules-based. The patchwork of industry-specific rules collapsed into one set of principles. The same five-step model applies whether you're a SaaS company, a contractor, or a hospital.

Performance obligations replaced "earnings process." Legacy GAAP recognized revenue when the earnings process was substantially complete and collection was reasonably assured. ASC 606 replaced that with the performance obligation construct, which is more granular and forces companies to decompose contracts into distinct units.

Variable consideration is in scope. Legacy GAAP generally deferred recognition of variable amounts (rebates, refunds, performance bonuses) until they became fixed and determinable. ASC 606 requires estimation up front, with a constraint that limits the estimate to what is highly probable not to reverse.

Contract costs can be capitalized. Under ASC 340-40 (introduced with ASC 606), incremental costs of obtaining a contract (sales commissions) can be capitalized and amortized over the contract life. Legacy GAAP generally expensed these as incurred.

Set-up fees and activation fees changed. Under SOP 97-2 and similar legacy rules, set-up fees were often deferred and recognized over the contract life. Under ASC 606, set-up fees are evaluated as a separate performance obligation. If the activity doesn't transfer a good or service to the customer, the fee is allocated across the underlying performance obligations.

Term-based software licenses recognize at a point in time. Under SOP 97-2, software revenue was often recognized over time. Under ASC 606, if a term-based license grants the customer the right to use the IP as it exists at the point of transfer, revenue is generally recognized at a point in time. This was one of the largest practical changes for software companies in 2018.

ASC 606 by industry: who got hit hardest

The transition was uneven. Retail companies that sell goods at a point of sale saw minimal change. Companies with long-term, complex contracts saw substantial rework.

Software and SaaS. The biggest impact. Set-up fees, term licenses, multi-element arrangements, usage-based pricing, and customer loyalty programs all changed treatment.

Telecom. Bundled handset-plus-service contracts had to be unbundled into separate performance obligations, with revenue allocated to each based on standalone selling price. This often meant recognizing handset revenue earlier (at delivery) and service revenue later.

Construction and engineering. Percentage-of-completion remains the dominant method, but ASC 606 forces a sharper distinction between input methods (cost-to-cost) and output methods (units completed, milestones).

Media and publishing. Bundled subscriptions, distribution rights, and license-of-content arrangements all got re-evaluated.

Healthcare. Charity care, variable consideration from third-party payors, and capitation contracts all required new estimation processes.

Retail. Minimal change for plain-vanilla point-of-sale transactions. Loyalty programs, gift cards, and warranties needed updates.

ASC 606 worked example: a B2B SaaS contract

A B2B SaaS company signs a four-year contract with a customer worth $6 million, paid upfront. The contract includes the SaaS subscription, a one-time set-up fee of $200,000, and unlimited support during the contract period.

Step 1: Identify the contract. The signed agreement, with payment terms, scope, and termination rights, is the contract.

Step 2: Identify performance obligations. Three candidates: SaaS access, set-up, support. Analysis: support is part of the SaaS service (not distinct in context), and set-up doesn't transfer a separate good or service to the customer (the customer can't take it elsewhere). The contract therefore contains one performance obligation: ongoing access to the SaaS platform.

Step 3: Determine the transaction price. $6,000,000.

Step 4: Allocate the transaction price. Single performance obligation, so the full $6 million is allocated to it.

Step 5: Recognize revenue. The SaaS service is delivered monthly over 48 months. The customer simultaneously receives and consumes the benefit, so revenue recognizes over time on a straight-line basis: $6,000,000 ÷ 48 = $125,000 per month, or $1,500,000 per year.

At contract signing, the company receives $6 million in cash. None of it is revenue yet. The full $6 million is recorded as deferred revenue (a liability) and recognized into revenue at $125,000 per month over the four-year term.

Now layer in variable consideration. Say the contract also includes a $500,000 performance bonus payable if the customer's NPS score exceeds 70 by year three. The company estimates a 60% probability of hitting the target, so the constrained variable consideration is $300,000. The transaction price rises to $6.3 million, and the monthly recognition becomes $131,250.

What is deferred revenue under ASC 606?

Deferred revenue (also called unearned revenue) is the liability recorded when a company receives payment before delivering the corresponding good or service. Under ASC 606, deferred revenue sits on the balance sheet until the performance obligation is satisfied. As revenue is recognized, the deferred revenue balance is drawn down.

For a SaaS company, deferred revenue is typically the largest current liability on the balance sheet and a key metric watched by investors. It represents committed future revenue that the company has been paid for but hasn't yet earned. Growing deferred revenue alongside growing recognized revenue is a sign of healthy contract bookings.

How Solvimon supports ASC 606 natively

Solvimon's Revenue primitive applies the five-step model automatically to every contract in the system. Each step maps to a specific primitive:

Step 1 (identify the contract) maps to Subscriptions and Subscription Schedules. Contracts, mid-term modifications, renewals, and amendments are all first-class objects with full audit history.

Step 2 (identify performance obligations) maps to Catalog and Entitlements. Products, plans, add-ons, features, and entitlements decompose every contract into its distinct components. Each component carries its own revenue recognition treatment.

Step 3 (determine the transaction price) maps to Pricing Models and Metering. Fixed fees, tiered pricing, usage-based fees, and variable consideration (rebates, performance bonuses, refunds) are tracked at the contract level. Variable consideration is estimated up front using configurable methods (expected value or most likely amount) with constraints applied per the standard.

Step 4 (allocate the transaction price) maps to Pricing Groups and Invoicing. Standalone selling prices are stored on the Catalog object and used to allocate transaction price across performance obligations automatically. Adjustments and corrections feed back into the same allocation engine.

Step 5 (recognize revenue) maps to the Revenue primitive. Recognition schedules are generated for every performance obligation at contract inception, posted to the deferred revenue ledger, and drawn down as the obligation is satisfied. Point-in-time and over-time recognition are both supported. Reports include the disclosures required under ASC 606-50 (contract balances, performance obligations, significant judgments) and the parallel disclosures required by IFRS 15 for international filers.

The result: a single ledger that produces ASC 606 revenue, IFRS 15 revenue (where the treatment differs), deferred revenue, and audit-ready support for both standards from the same source of truth. No bolt-on revenue recognition tool. No reconciliation across systems.

Related terms

Deferred revenue (unearned revenue)

Frequently Asked Questions

When did ASC 606 become effective?

ASC 606 became effective for public companies in fiscal years beginning after December 15, 2017, and for private companies in fiscal years beginning after December 15, 2018. Most public companies adopted it for the year ended December 31, 2018.

What's the difference between ASC 606 and IFRS 15?

ASC 606 (US GAAP) and IFRS 15 (IASB) share the same five-step model and produce nearly identical results in most cases. Differences include the threshold for "probable" collectibility (75-80% under US GAAP, more likely than not under IFRS), policy elections for shipping and sales taxes, and disclosure depth.

Does ASC 606 apply to private companies?

Yes. ASC 606 applies to all entities, public or private, that enter into contracts with customers for the transfer of goods or services. Private companies were given an extra year for adoption (fiscal years after December 15, 2018).

What's a performance obligation?

A performance obligation is a promise in a contract to transfer a distinct good or service to a customer. A single contract can contain one or many performance obligations, and each one gets its own revenue recognition treatment under the five-step model.

How does ASC 606 affect SaaS companies?

SaaS companies were among the most affected industries. Set-up fees, term licenses, multi-element arrangements, usage-based pricing, and customer loyalty programs all changed treatment. The biggest practical impact: SaaS subscriptions recognize over time, but term-based perpetual licenses now often recognize at a point in time.

What's the difference between ASC 606 and ASC 605?

ASC 605 was the legacy US GAAP revenue standard, alongside SAB 104, SOP 97-2, and industry-specific rules. ASC 606 replaced all of them with a single principles-based standard. The biggest conceptual change: ASC 606 uses performance obligations and recognizes revenue when control transfers, while ASC 605 used the "earnings process" model.

What's deferred revenue under ASC 606?

Deferred revenue (or unearned revenue) is the liability a company records when it receives payment before delivering the corresponding good or service. Under ASC 606, deferred revenue is recognized into revenue as the underlying performance obligation is satisfied.

Do I need ASC 606 if I use cash-basis accounting?

ASC 606 applies to entities that prepare financial statements under US GAAP, which is accrual-based. Pure cash-basis taxpayers (typically very small businesses) don't apply ASC 606 to their tax accounting. Any company audited under US GAAP applies the standard.

What's the difference between point-in-time and over-time revenue recognition?

Over-time recognition spreads revenue across the period during which the customer receives the benefit (typical for SaaS, services, long-term construction). Point-in-time recognition records all the revenue at the moment control transfers (typical for product sales, term-based perpetual licenses). The standard provides specific criteria for which method applies.

How does ASC 606 handle multi-element arrangements?

Multi-element arrangements are decomposed into distinct performance obligations under Step 2. The transaction price is then allocated across them using standalone selling prices under Step 4, and each performance obligation gets recognized on its own schedule under Step 5.

Does ASC 606 affect SaaS metrics like ARR or MRR?

ASC 606 governs financial-statement revenue (GAAP revenue). ARR and MRR are operational metrics that may or may not align with GAAP revenue depending on how a company defines them. Most SaaS companies report both, with reconciliation between the two.

Solvimon's Revenue primitive supports ASC 606 and IFRS 15 from a single ledger.

Ready for billing v2?

Solvimon is monetization infrastructure for companies that have outgrown billing v1. One system, entire lifecycle, built by the team that did this at Adyen.

Price Benchmarking

AI Token Pricing

Freemium Model

Market Based Pricing

Odd-Even Pricing

Price Estimation

Marginal Cost Pricing

Quote to Cash

Revenue Assurance

ASC 606

Revenue Recognition

ACH

Subscription pause

Entitlements

France's E-Invoicing reform

E-invoicing

Net Revenue Retention: How to Calculate It and What It Actually

Volume Commitments

IFRS 15

Prepaid vs Postpaid billing

PLG billing

Captive Product

Headless Monetization

Seat-based Pricing

Usage-based Pricing

Invoice

MRR & ARR

Subscription Management

Recurring Payments

Cost Plus Pricing

Dunning

Payment Gateway

Value Based Pricing

Revenue Backlog

Deferrred Revenue

Consolidated Billing

Pricing Engine

Embedded Finance

Overage Charges

Flat Rate Pricing

Minimum Commit

Yield Optimization

Grandfathering

Billing Engine

Predictive Pricing

Metering

AI Agent Pricing

AI-Led Growth

AISP

Advance Billing

Credit-based pricing

Outcome Based Pricing

Top Tiered Pricing

Region Based Pricing

High-Low Pricing

Lifecycle Pricing

Pay What You Want Pricing

Time Based Pricing

Contribution Margin-Based Pricing

Decoy Pricing

Dual Pricing

Loss Leader Pricing

Omnichannel Pricing

Revenue Optimization

Sales Enablement

Sales Optimization

Volume Discounts

Margin Management

Sales Prediction Analysis

Pricing Analytics

Intelligent Pricing

Margin Pricing

Price Configuration

Customer Profitability

Discount Management

Dynamic Pricing Optimization

Enterprise Resource Planning (ERP)

Guided Sales

Margin Leakage

Usage Metering

Smart Metering

Quoting

CPQ

Self Billing

Revenue Forecasting

Revenue Analytics

Total Contract Value

Pricing Bundles

Penetration Pricing

Dynamic Pricing

Price Elasticity

Feature-Based Pricing

Transaction Monitoring

Minimum Invoice

Tiered Pricing

SaaS Billing

Billing Cycle

Payment Processing

Hybrid Pricing Models

Stairstep Pricing

Multi-currency Billing

Multi-entity Billing

Ramp Up Periods

Proration

Sticky Stairstep Pricing

Tiered Usage-based Pricing

Revenue Leakage

PISP

PSP

Why Solvimon

Helping businesses reach the next level

The Solvimon platform is extremely flexible allowing us to bill the most tailored enterprise deals automatically.

Ciaran O'Kane

Head of Finance

Solvimon is not only building the most flexible billing platform in the space but also a truly global platform.

Juan Pablo Ortega

CEO

I was skeptical if there was any solution out there that could relieve the team from an eternity of manual billing. Solvimon impressed me with their flexibility and user-friendliness.

János Mátyásfalvi

CFO

Working with Solvimon is a different experience than working with other vendors. Not only because of the product they offer, but also because of their very senior team that knows what they are talking about.

Steven Burgemeister

Product Lead, Billing